Last August, we informed you that President Obama signed into law the Flood Insurance Reform Act, which introduced changes to the National Flood Insurance Program (NFIP). The legislation was implemented to improve efficiency of the program while equipping FEMA with resources needed to update the country’s flood maps. In addition, the Flood Insurance Reform Act introduced measures that would help the program become solvent, such as eliminating subsidized insurance rates for properties with repeated flood claims. According to FEMA, “Key provisions of the legislation will require the NFIP to raise rates to reflect true flood risk, make the program more financially stable, and change how Flood Insurance Rate Map (FIRM) updates impact policyholders. The changes will mean premium rate increases for some – but not all – policyholders over time.” With the 2013 fiscal budget constraints and recent sequester measures, it appears that FEMA will receive even less funding than in previous years. The slashed funding may ultimately set back the program 5 to 7 years and leave many Americans with outdated flood maps that do not represent the true level of risk.

Saga of outdated flood maps continues

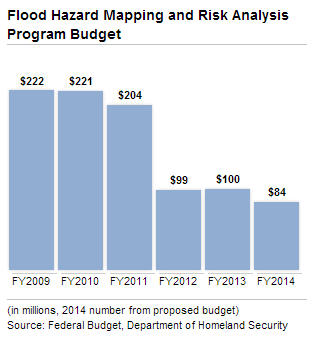

According to an article published by ProPublica, “As part of an overhaul to the insurance program last year, Congress authorized the government to spend $400 million a year for the next five years to update flood maps. But for the 2013 fiscal year, Congress has appropriated just a quarter of that amount. Sequestration has cut another $5 million, according to the Office of Management and Budget, leaving $95 million for flood mapping this year.” Officials have predicted that the program would probably require upwards of $4 billion over the next decade in order to accomplish FEMA’s goal of getting 80 percent of the country’s flood data up-to-date.

According to an article published by ProPublica, “As part of an overhaul to the insurance program last year, Congress authorized the government to spend $400 million a year for the next five years to update flood maps. But for the 2013 fiscal year, Congress has appropriated just a quarter of that amount. Sequestration has cut another $5 million, according to the Office of Management and Budget, leaving $95 million for flood mapping this year.” Officials have predicted that the program would probably require upwards of $4 billion over the next decade in order to accomplish FEMA’s goal of getting 80 percent of the country’s flood data up-to-date.

How does the forecast look?

Not long after passage of the new act, Hurricane Sandy flooded over 100,000 homes and strained the NFIP even further. It is estimated that damages caused by Sandy could reach more than $7 billion, but the program is only allowed to add $3 billion to its current debt, likely leaving taxpayers to make up the difference. Additionally, with the new act requiring homeowners in flood prone areas to meet stricter building codes, many are left calculating the costs and trying to determine if rebuilding is an economically viable option. It seems to me that legislatures on both sides of the aisle need to get serious about properly distributing funding to FEMA so they can successfully do their job – a job that is fundamental in assessing risk not only to property damage but also risk to human life.

Even though the NFIP is facing debt that the program cannot lawfully take on, there is a glimmer of light at the end of the tunnel. With new rules coming into effect, rates will eventually rise to levels that accurately reflect risk and hopefully make the program solvent. With new requirements in place, both new and rebuilt homes must be modernized to better withstand flood conditions. Inevitably, we will continue to experience hurricanes and property loss from flooding, but if the program reforms are successful, the NFIP will be in a better position to anticipate and respond to these forces, thanks to a program that is more responsibly designed to deal with the natural disasters of tomorrow.

Jordan Schmidt

Editor

jschmidt@banksinfo.com

Image source: ProPublica